Carbon Border Adjustment Mechanism (CBAM) Quantification Service

Quantify your product's carbon emission to ensure compliance with the EU's CBAM requirements, where inaccurate or delayed reporting can result in financial penalties and reputational damage.

To calculate a Carbon Border Adjustment Mechanism (CBAM) cost, you'll need:

- The weight of the imported good (in tonnes)

- The embedded greenhouse gas (GHG) emissions factor (in tonnes of CO₂ equivalent per tonne of good), and

- The average weekly EU ETS price (in euros per tonne of CO₂ equivalent).

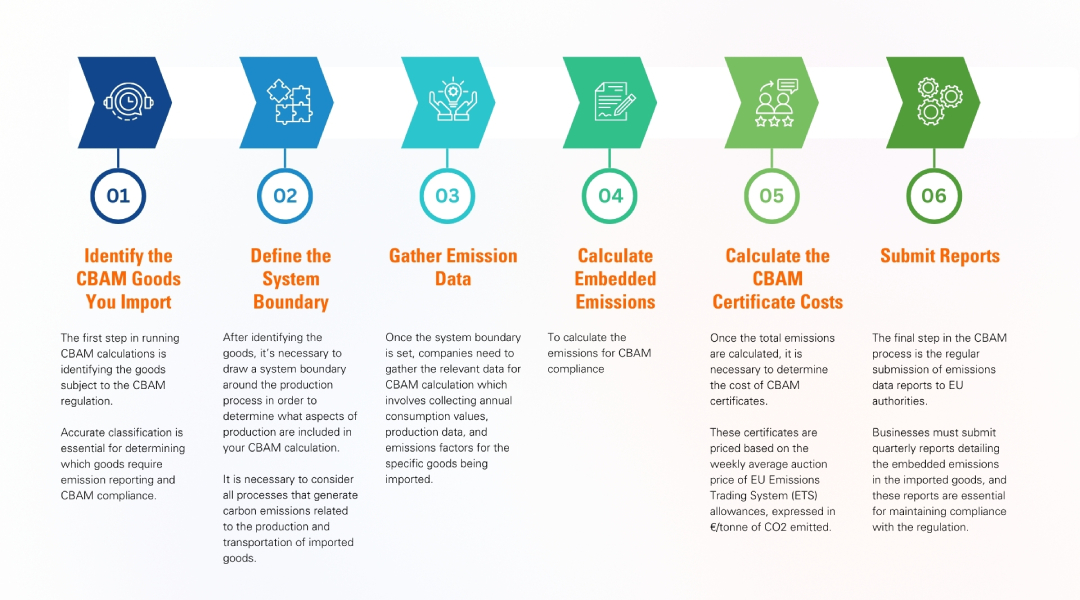

A simple 5-step approach to kick-start the process:

What is the Carbon Border Adjustment Mechanism (CBAM)?

The Carbon Border Adjustment Mechanism (CBAM) is a regulatory tool that applies a price at the EU border on the greenhouse gas content of imported products, which matches the carbon price paid for similar products produced in the EU.

Its introduction is a response to concerns that increasing internal EU carbon prices risks creating a competitive disadvantage for EU producers on the European Single Market, compared to non-EU producers that don’t have to pay a carbon price. This might result in decreased EU production or lead to relocation to a country without a carbon price. Although this would reduce domestic emissions, it could result in increased emissions elsewhere. This potential outcome is known as “carbon leakage”, and its prevention was the primary reason for the introduction of CBAM within the Fit-for-55 Package.

What sectors and emissions does the CBAM cover?

CBAM will cover imported cement, iron and steel, aluminium, fertilizers, electricity, and hydrogen, arriving from outside the EU. For each sector, a list of classified products has been selected based on Combined Nomenclature (CN) codes.

CBAM covers both direct and (only for cement and fertilizers) indirect emissions. Direct emissions are released during the production – and are defined as Scope 1. Indirect emissions refer to emissions occurring from the electricity used during production, and are described as Scope 2 emissions. Direct and indirect emissions of relevant precursors (the raw materials used in the production of complex goods) are also taken into account when calculating the carbon intensity of CBAM products.

How are emissions calculated under CBAM?

- Default values:

- For part of the transitional reporting period, CBAM declarants used global default values as set by the European Commission with the support of the Joint Research Centre. For the definitive period, the Commission will set default values by country (and even by region) informed by the data collected during the transitional reporting period. Otherwise, “best available data” based on reliable and publicly available information will be used, and revised periodically through implementing acts, according to Annex IV (4).

- Actual emissions:

- For industrial products, Annex IV (2-3) lays out the calculation methodologies of embedded emissions – taking into account the total emissions of goods (simple or complex) and the activity level (quantity of goods produced) during the reporting period.

Article 7 of the Regulation empowers the Commission to adopt implementing acts to flesh out the details of these methodologies.

Are there any exemptions?

The proposal includes three types of exemptions:

- Countries outside the EU but participating in the EU ETS, and countries with carbon markets linked to the EU ETS, are excluded from CBAM (EEA countries, Switzerland).

- If a third country has an electricity market that is integrated with the EU internal market for electricity through market coupling, and it has not been possible to find a technical solution for applying the CBAM to electricity imports in the EU, the importation of electricity from the country will be exempted from the application of the CBAM, provided certain corresponding conditions are satisfied.

- Finally, the “force majeure” clause in Article 30 states that where an unforeseeable, exceptional and unprovoked event has occurred that is outside the control of third countries subject to the CBAM, and that event has destructive consequences on their economic infrastructure, the Commission shall submit a report to the co-legislators, accompanied, where appropriate, by a legislative proposal setting out the necessary provisional measures to tackle the situation.