How does the CBAM work?

The CBAM has been designed to comply with the EU’s international commitments and obligations, including World Trade Organization (WTO) rules. The CBAM system mirrors the EU ETS and works as follows:

- CBAM is applied to the actual embedded emissions in the goods imported in the EU, determined according to a methodology that is in line with the reporting of emissions under the EU ETS for the production of similar goods in the EU

- As of the entry into force of the definitive period of CBAM in 2026, EU importers will buy CBAM certificates corresponding to the carbon price that would have been paid, had the goods been produced under the EU's carbon pricing rules.

- Conversely, if a non-EU producer has already paid a carbon price in a third country on the embedded emissions for the production of the imported goods, the corresponding cost can be fully deducted from the CBAM obligation.

The CBAM will therefore help reduce the risk of carbon leakage while encouraging both producers in non-EU countries to green their production processes, as well as countries to introduce carbon pricing measures.

To provide businesses and other countries with legal certainty and stability, the CBAM is being phased in gradually and initially applies only to a selected number of goods in sectors at high risk of carbon leakage. In the transitional period, which started on 1 October 2023, a reporting system applies for those goods with the objective of facilitating a smooth rollout and facilitating dialogue with third countries. Importers will start paying the CBAM financial adjustment in 2026.

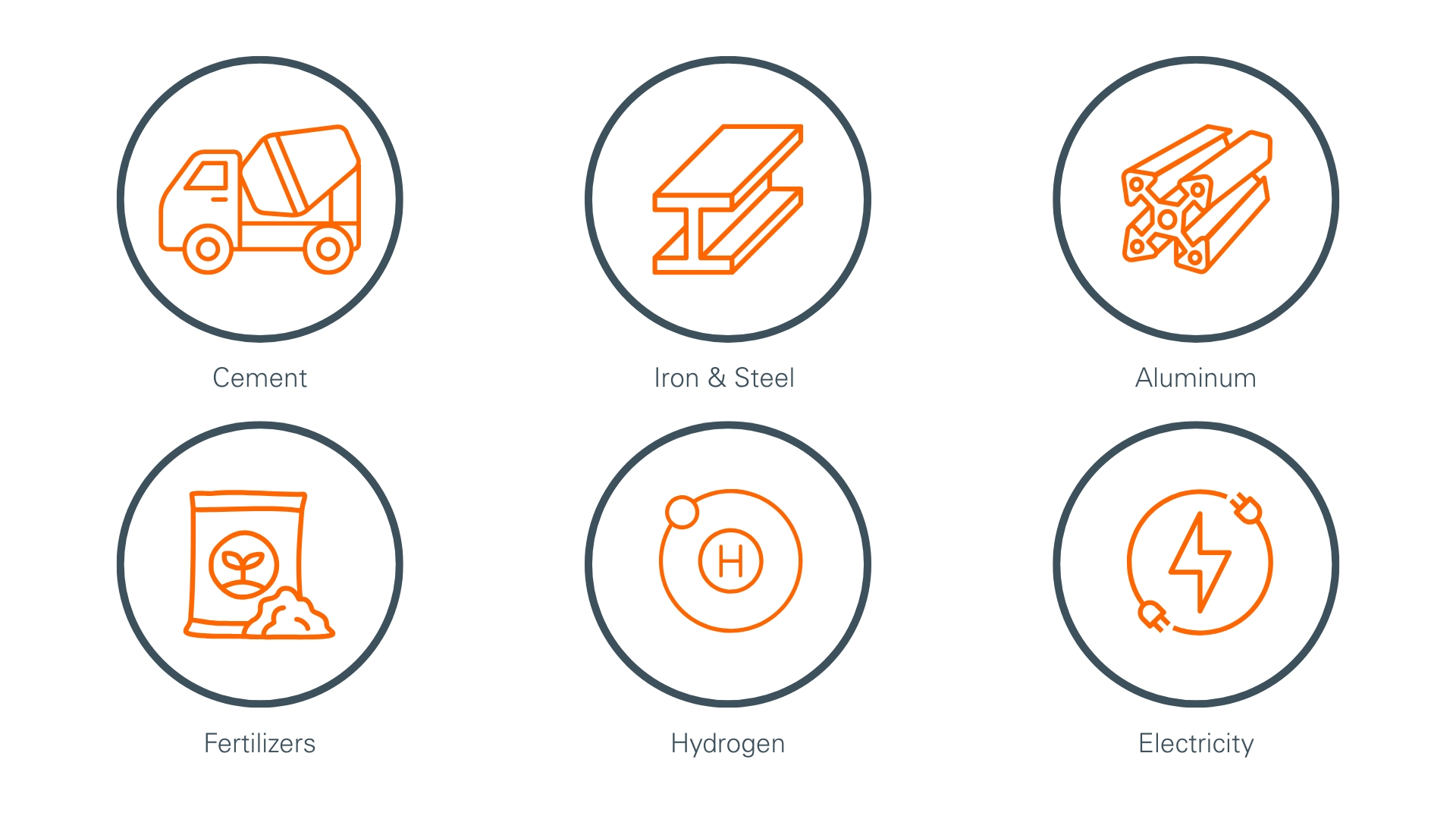

Which sectors does the new mechanism cover, and why were they chosen?

The CBAM initially applies to imports of the following goods:

These sectors were selected following specific criteria, in particular their high risk of carbon leakage and high emission intensity, which will eventually, once fully phased in, represent more than 50% of the emissions of the industry sectors covered by the ETS. In the future, the CBAM may be extended to other ETS sectors.

How does CBAM interact with the EU Emissions Trading System (ETS)?

The CBAM will be based on a system of certificates corresponding to embedded emissions in CBAM products imported into the EU. The CBAM departs from the ETS in some limited areas where it was needed, as it is not a ‘cap and trade' system. For example, unlike the EU ETS, an unlimited number of certificates can be purchased. Nevertheless, the price of CBAM certificates will mirror the ETS allowance price.

Once the full CBAM regime becomes operational in 2026, the system will adjust to reflect the revised EU ETS, in particular when it comes to the reduction of available free allowances in the sectors covered by the CBAM. This means that the CBAM will only begin to apply to the products covered, and in direct proportion to the reduction of free allowances allocated under the ETS for those sectors. Simply put, until free allowances in CBAM sectors are completely phased out in 2034, the CBAM will apply only to the proportion of emissions that does not benefit from free allowances under the EU ETS, thus ensuring that importers are treated in an even-handed way compared to EU producers.

Are there penalties for non-compliance with the CBAM Regulation?

Yes. Reporting of embedded emissions in CBAM goods from 1 October 2023 is compulsory. Reporting declarants may face penalties ranging between EUR 10 and EUR 50 per tonne of unreported emissions. The penalties apply where:

- The reporting declarant has not taken the necessary steps to comply with the obligation to submit a CBAM report, or

- Where the CBAM report is incorrect or incomplete, and the reporting declarant has not taken the necessary steps to correct the CBAM report after the competent authority initiated the correction procedure

What are the reporting obligations? By when do I need to submit a report?

During the transitional period of the CBAM, from 1 October 2023 until 31 December 2025, the importer shall submit a CBAM report on a quarterly basis. This report shall include the information on the goods imported during the previous quarter and should not be submitted later than one month after the end of that quarter. The reporting calendar during the transitional period is outlined below:

The report shall include the information referred to in Article 35 of the Regulation:

- The total quantity of each type of CBAM good;

- The actual total embedded emissions;

- The total indirect emissions;

- The carbon price due in a country of origin for the embedded emissions in the imported goods (including its relevant precursors where applicable), taking into account any rebate or other form of compensation available

How can SGS help?

We are market leaders in EU ETS verification across all CBAM-covered sectors. SGS offers a range of CBAM services to help you meet the requirements, such as: